Most business owners assume their tax bill is just a cost of doing business. You earn money, the government takes its share, and whatever’s left is yours to work with. If the margins are thin, that’s a revenue problem. Or an expenses problem. Or a pricing problem. The answer is always to do more — sell more, cut more, push harder.

But what if the problem isn’t any of those things?

What if a significant portion of the money you’re leaving on the table is sitting quietly inside the U.S. tax code, already designated for businesses exactly like yours — and nobody told you it was there?

That’s the reality for the majority of companies that qualify for the Research and Development (R&D) tax credit. It’s not a loophole. It’s not aggressive tax planning. It’s a legitimate federal credit that Congress created specifically to reward American businesses for building things, solving problems, and improving processes. And according to IRS data, roughly 70% of businesses that qualify for it never claim it.

Not because they don’t deserve it. Because they don’t know it exists.

To understand what that actually means in practical terms, let’s walk through five data points using a single $2M engineering company as our example. Same business throughout. Same $2,000,000 in revenue. Same $1,950,000 in expenses. The only thing that changes is whether the R&D tax credit has been applied.

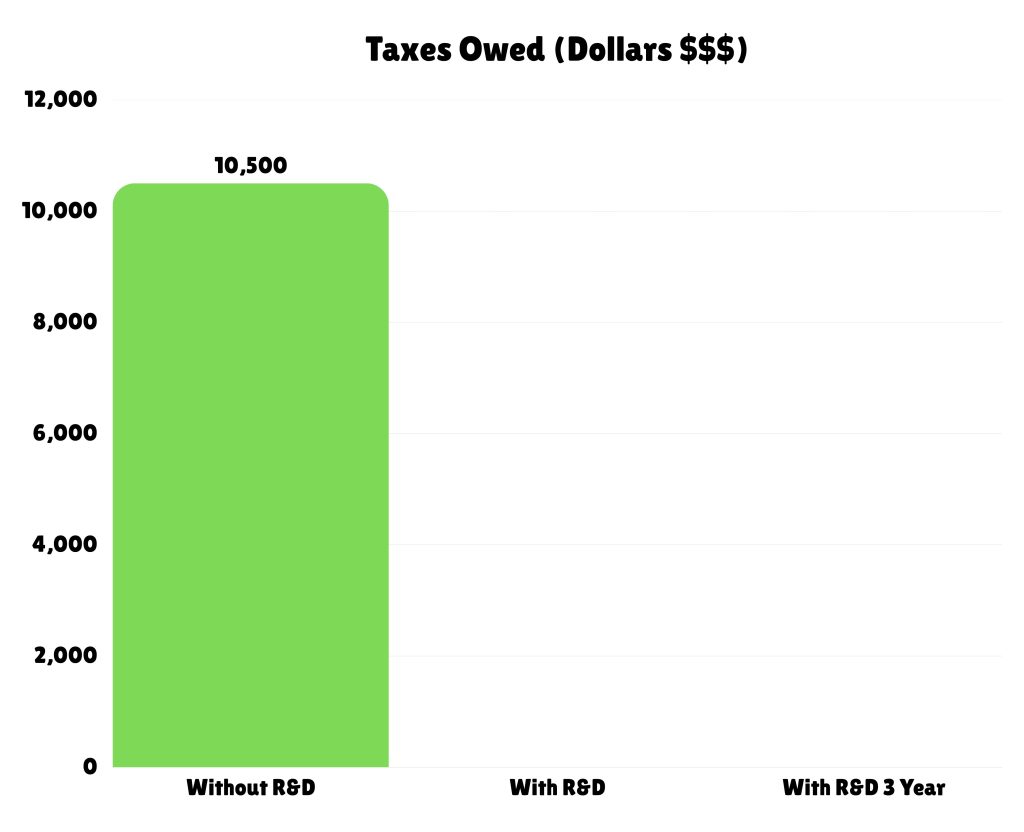

The Tax Burden

Before anything else, let’s look at the tax picture in its most basic form.

Without the R&D credit, this company’s $50,000 in profit gets taxed at the standard corporate rate. The result: a tax bill that consumes most of what was left, bringing actual after-tax cash down to approximately $39,500. That’s a real-world margin of 1.9% on $2,000,000 in revenue.

Now look at the same company with the R&D tax credit applied. The credit doesn’t just reduce the tax bill — for many qualifying businesses, it eliminates it entirely. When that bar drops to zero, everything that was going to the IRS stays in the business instead.

This is where most conversations about the R&D credit begin and end. But the tax liability is only one piece of the picture.

Payroll Tax Savings

Here’s the part that surprises most people.

The R&D tax credit isn’t limited to reducing income tax. For qualifying small businesses — generally those with under $5 million in gross receipts and less than five years of revenue — a portion of the credit can be applied directly against the employer’s payroll tax obligation. This is a provision that was significantly expanded by the Protecting Americans from Tax Hikes (PATH) Act, and it’s one of the most underutilized mechanisms in the entire tax code.

For our $2M engineering company, this translates to $40,000 in annual payroll tax savings — on top of the eliminated income tax liability. And unlike many tax benefits, this one doesn’t depend on being profitable. Even in a year where the business breaks even or runs at a loss, the payroll credit can still be claimed.

That’s $40,000 back into operations. Every year. Without changing a single thing about how the business runs.

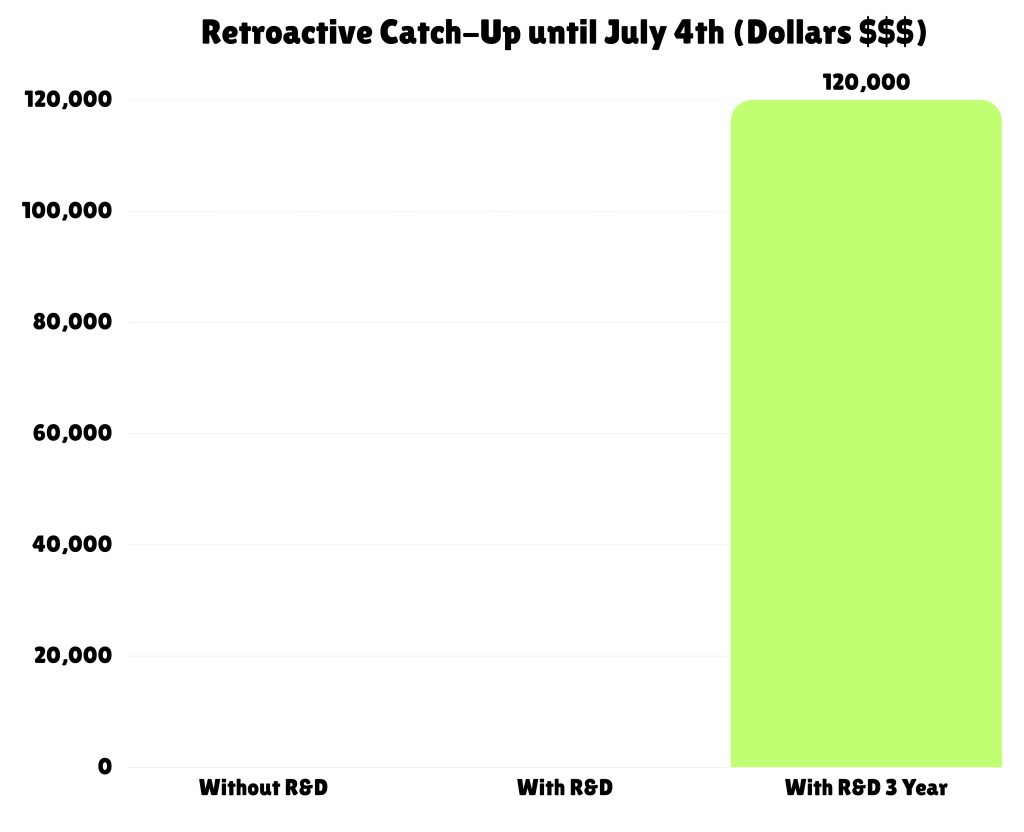

The Retroactive Catch-Up Window

This is where the conversation shifts from “annual benefit” to “immediate recovery.”

Most business owners don’t realize that the IRS allows companies to go back and amend prior year returns to claim credits they were eligible for but never filed. The window for doing so is three years. That means if your business has been qualifying for the R&D credit — and operating without it — you may be sitting on a significant amount of recoverable cash from years you’ve already closed the books on.

For our example company, three years of unclaimed credits adds up to $120,000 in recoverable funds. This isn’t new money. It’s not a bonus or a windfall. It’s money this business already earned, already paid taxes on, and is now legally entitled to recover. The IRS has a mechanism for it. The process exists. It just requires someone to file it correctly.

The critical detail here is timing. The retroactive window is currently open — but it closes July 4th. After that date, any credits from the eligible prior years are permanently forfeited. The annual credit going forward remains available, but the catch-up window does not reopen. For a business sitting on $120,000 in recoverable credits, that deadline is not abstract. It is a hard cutoff with a real dollar figure attached to it.

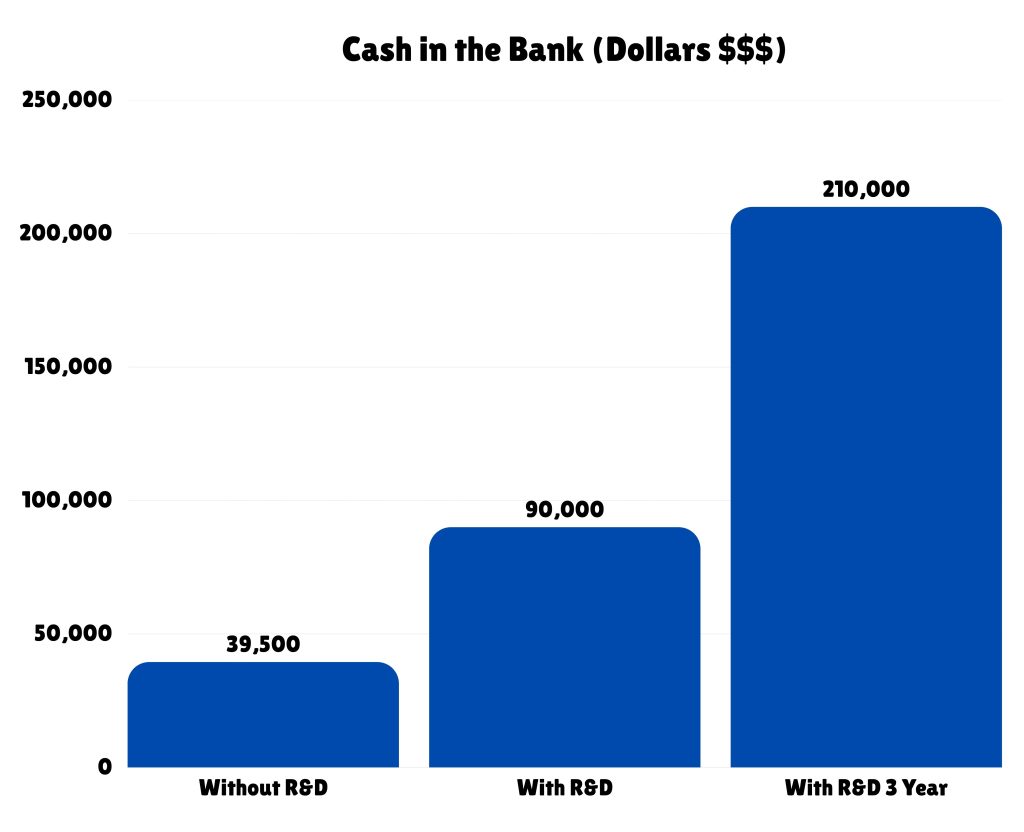

Cash in the Bank

Now let’s step back and look at what all of this means for the number that actually matters to a business owner on a day-to-day basis: cash in the bank.

Three versions of the same company. Same revenue. Same expenses. Same team.

Scenario 1 — No R&D credit: After taxes, the business retains $39,500. This is the reality for most companies in this position. It’s functional, but there’s no buffer. One slow quarter, one unexpected expense, one client that pays late — and the year is essentially lost.

Scenario 2 — Annual R&D credit applied: The tax liability is eliminated and payroll savings are captured. Cash in the bank jumps to $90,000. That’s more than double — without touching revenue, without cutting a single expense, without adding a single client. The business didn’t get better at what it does. It got better at keeping what it earns.

Scenario 3 — Annual credit plus retroactive recovery: The $120,000 catch-up from prior years stacks on top. Total cash position: $210,000. The business now has a financial cushion that changes what’s possible — whether that’s hiring, equipment, marketing, or simply sleeping better at night knowing the business can weather a bad stretch.

The bars in that graph represent the same company at three different points of tax strategy. The gap between the first bar and the third isn’t a matter of hustle or market conditions. It’s a matter of information.

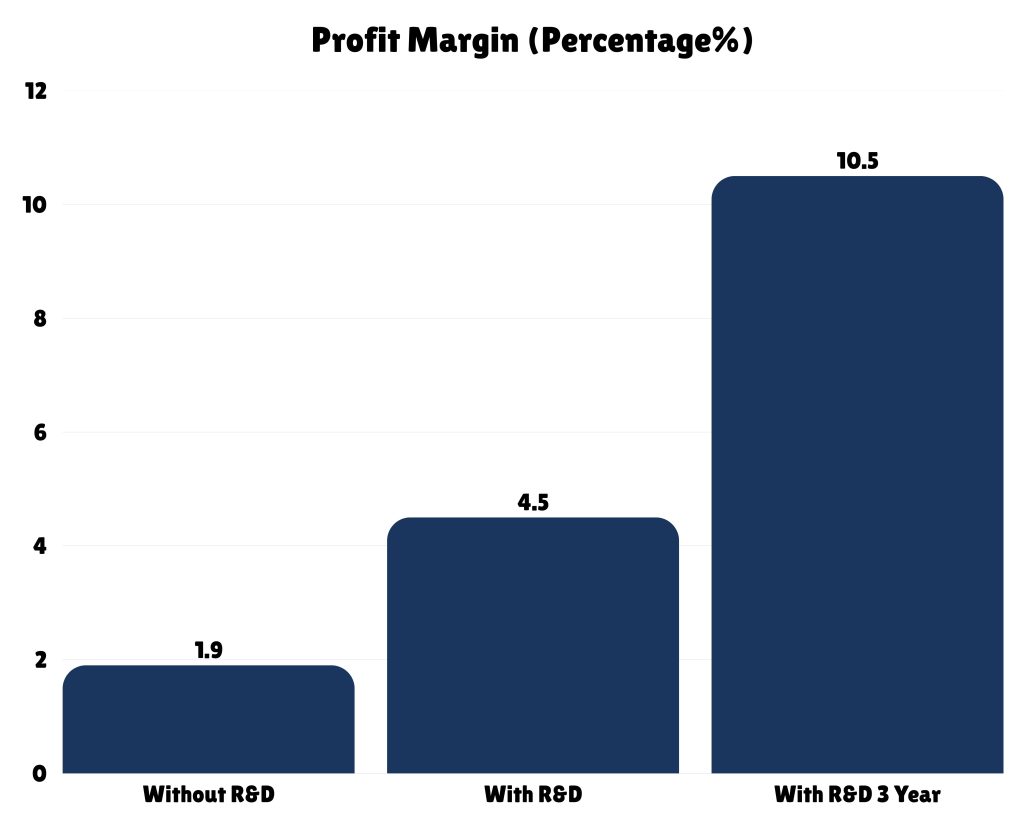

Profit Margin

Margin is how you measure whether a business is truly healthy — and it’s the number most owners try hardest not to think about.

A 1.9% margin is not a business that’s winning. It’s a business that’s surviving, and only barely. At that margin, every variable is a threat. Losing a key employee, an equipment failure, a delayed contract — any one of those things can erase the year. Business owners at 1.9% often describe a persistent feeling that no matter how hard they work, the bank account never quite reflects it. That feeling is accurate. The math confirms it.

A 4.5% margin — the result of the annual R&D credit alone — is meaningfully different. It’s not a dramatic transformation, but it’s the difference between a business that reacts to every problem and one that can begin to build intentionally.

A 10.5% margin is a different category of business entirely. At 10.5%, you can reinvest, you can plan, you can absorb setbacks without catastrophizing. You can start operating like the 30% of businesses that are genuinely building something — rather than grinding to maintain what you have.

Who Actually Qualifies?

The R&D tax credit has a reputation for being a Silicon Valley benefit — something for biotech companies and software labs with PhDs on staff. That reputation is wrong, and it’s one of the reasons so many qualifying businesses never pursue it.

The credit applies to any business that engages in activities that qualify as research or experimentation under IRS Section 41. In practice, that includes developing or improving products, designing custom systems, engineering solutions to technical problems, writing software, improving manufacturing processes, and testing new methodologies. Engineering firms, construction technology companies, food manufacturers, healthcare technology providers, and countless others qualify every year — and most of them don’t know it.

The IRS doesn’t require you to have a formal R&D department. It doesn’t require patents or published research. It requires that your business engaged in activities that involved technical uncertainty, a process of experimentation, and a technological purpose. For many companies, that describes a significant portion of what they do every day.

The Next Step

If you looked at those five graphs and recognized your business in the first set of bars, the most valuable thing you can do right now is find out where you actually stand.

Quartermaster Tax offers a free 20-minute eligibility call. We’ll look at your specific situation — your industry, your activities, your prior filings — and tell you straight up what you qualify for and what the numbers look like for your business. No obligation. No upsell. Just clarity.

The retroactive window closes July 4th. The annual credit is available every year going forward. Both of them are worth understanding before you file another return without them.

Click here to book your free 20-minute eligibility call with Quartermaster Tax.